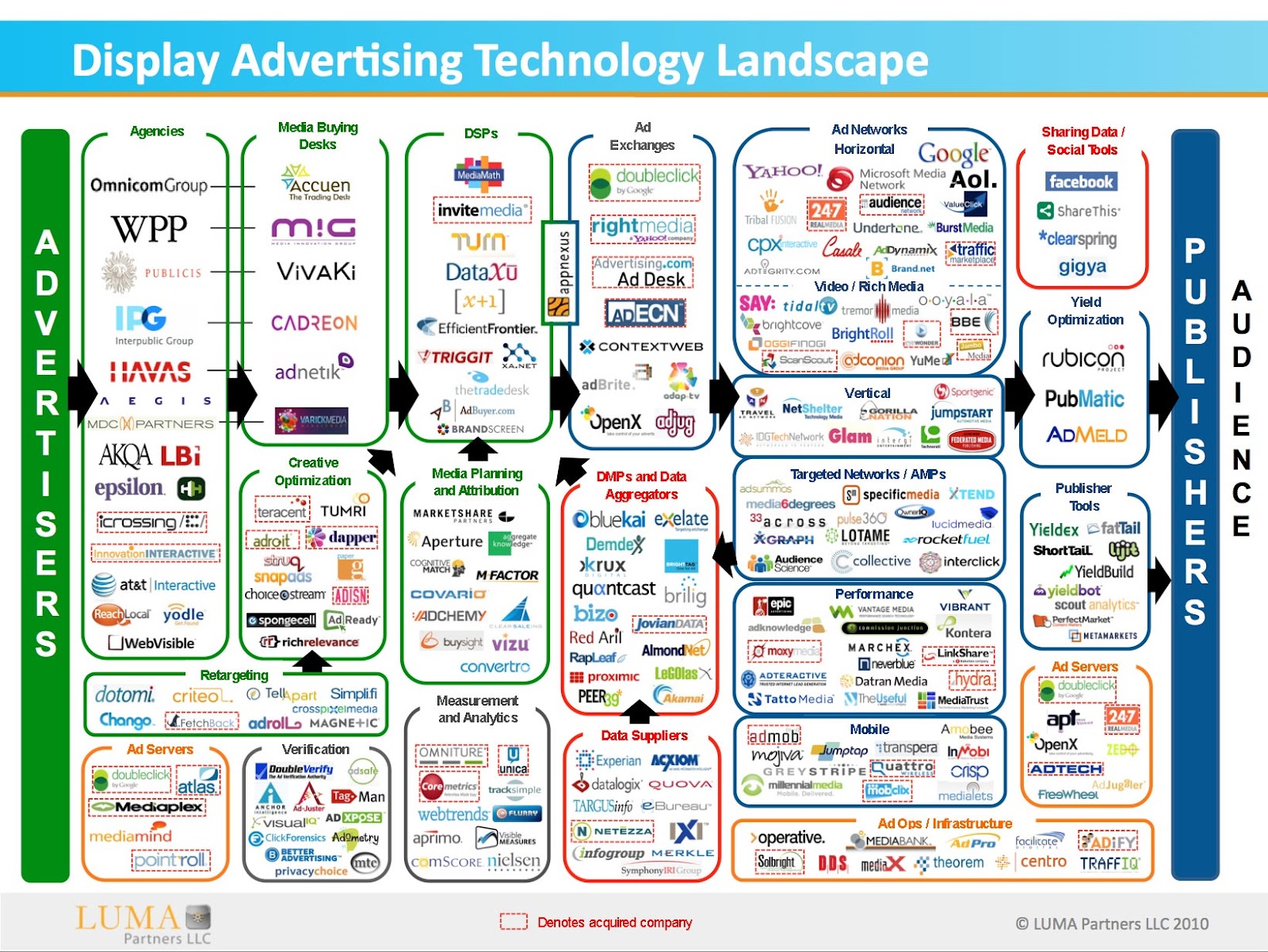

Spring is upon us and many of us are coming from and going to conferences this week. With so many interesting events to chose from it is exciting to see all the innovations and industry continuing to grow; analyst Jack Myers put digital advertising at $47.6 Billion last year (8% share of total marketing spend). This is no doubt evidenced by the plethora of technology companies captured in Terrence Kawaja’s ubiquitous

Display Advertising Landscape diagram. Yet, the colorful framework belies the complex and fierce co-evolution that is happening behind-the-scenes of the so-called

Ad Technology Stack.

Focused on hitting their milestones and/or quotas, investor-fueled and publicly-traded ventures alike will be putting on the hard-sell this trade show season. Panel and exhibit hall attendees certainly know the drill. Prospects will be dazzled, plans hatched and hopes dashed with the latest BSO (bright shiny object) hanging in the balance. On tap across booth chit-chat, panel pontification, martinis and outdoor activities will be information (not to mention outright disinformation). Perpetual conversion machines are the latest rage!

After years of consolidation and financial speed bumps the current industry, while seeing more revenue has definitely shrunk in terms of choices. It should not be a surprise that many battle-scarred survivors have benefitted from this and effective technology lock-in strategies. The result for some technology buyers has been worse service levels and slowed innovation. Nonetheless, gaps in the incumbent’s vision or their inability to consistently innovate have spawned mini-me’s up and down the stack; some trying to create their own lock-in. Unfortunately, all this has all been accepted as a cost of doing business.

To buyers of stack technologies: caveat emptor.

We Know What You’re Up To

Once the technology deal is done – it is going to be too late. Control immediately begins to shift from the technology buyer to the seller. Why does leverage shift? In economic terms, the buyer may have just unwittingly entered into a deal with a micro-monopolist. While this could be arguably true for many industries, for stack buyers this has more severe consequences. The kind that are often obfuscated yet pervasive and only become fully understood in time. It goes way beyond simple buyer’s remorse.

Ad Technology Stack business models that rely on technology lock-in do so because their investors and management have found that such switching inflexibility works for them. One need only look around to find many mainfestations across the stack, mainly in two areas:

- Performance analytics – ownership, access and control of reporting data

- Behavioral data – for both advertisers and publishers

Due to information asyncronicity, technology buyers often don’t realize fast enough that they are really signing up to purchase a series of products and services -all when they are at the greatest informational disadvantage. As a result, stack buyers can easily become captives of their own making. A little diligence and research upfront can mitigate the common self-inflicted damage caused by lock-in.

Switching Cost and Lock-in

In game theory, a product or service has a switching cost when the buyer purchases it over multiple periods of time and experiences time, cash or opportunity costs to switch from one seller to another. Switching costs can also occur when a buyer purchases additional complementary products or services making substitutes relatively more expensive; increased complexity is positively correlated with higher switching costs.

Altogether this effectively shifts the supply curve and creates the “lock-in” effect thus raising costs for the buyer. Clearly, switching items in the stack can have unintended negative consequences. More specifically, when a businesses contracts with a stack company there are usually multiple economic components to what is effectively the total cost of ownership (TCO):

- Implementation

- Learning Curve:

- Application usage

- Report data warehousing

- Framework

- Contractual

- Network considerations

- Opportunity

All of the above combine to create an effective transaction or cost of switching. Although implementation is an obvious one-time cost (sometimes the largest component), other costs are more subtle and may actually increase over time. Practical scenarios might include:

- changing the ad server or site analytics technology

- managing research or targeting page tags (and data sharing)

Staying Balanced in the Melee

While the lock-in strategy has worked well for technology sellers in the past, many Ad Technology Stack ventures are about to get their legs kicked from under them. Enter tag (data) management companies like BrightTag, Tagman, Ensighten and Tealium.These companies are exclusively, if not mostly focused on managing proliferating page tags which are a major culprit behind stack lock-in. Having one technology locked-in that you’ve planned for is probably better than fifteen that just happened over time.

In addition to to making the business of digital marketing actually manageable from a logistical tag and data-sharing standpoint, the larger possibilities are tantalizing for stack buyers wrestling with IT/development queues. Simply put, tag management changes the balance of leverage away from the sellers towards their customers. Analytics expert, Eric Peterson called this out in a recent white paper saying:

“…as implementations become more involved and sophisticated the businesses willingness to switch vendors declines, even in situations where the relationship has been badly damaged by miss-set expectations, miscommunication, or outright lies”

Fear and Loathing

Yes, positive change is in the air for the industry. Widespread use of tag management systems make this an inevitability. However, reactions span the contninuum:

- Guarantee us business and we’ll integrate

- These companies are risky start-ups

- We have developed our own solution

- Interesting, but never heard of it

- No problem, we can work with anyone

- Great idea, we want to get to market first

No wonder that the reactions from the ad technology stack about universal tag management have been mixed – these tag management companies are upsetting the status quo and threatening lock-in!

Laggards are doing what they do: delaying and holding out. They are not happy about this. Some are attempting to make tying deals to lock-in even more. For this desperate and unimaginative bunch, it will be a slow and steady burn as the balance of power swings back; some may even get crushed. Others will respond by acquiring companies or being acquired. Still others will hit the wall or just become irrelevant.

More proactive technology sellers see this as an opportunity for competitive advantage and customer relationship-building. This breed of stack company is already knows how to adapt to the new reality of constantly being tested. They are fast failers and built to optimize, now using the opportunity to proactively to gain compeititve advantage.

Moving Forward

Technology stack buyers must balance the fear of being left-behind with a more reasoned approach. Sellers must be able to provide value today without depending on technology lock-in to be successful in the long-term; management discipline and technology agility are essential.

On the upside, one promising trend is that for the first time since the implosion of the Web 1.0 industry, business development (not strategic sales execs) executives are popping up across Ad Technology Stack start-ups. Having the organizational competency to vet and manage strategic alliances is a step in the right direction. Kudos.

Interoperability matters. Compatibility across the stack is a must-have and stack players that didn’t learn the lessson of Betamax (in hopes of another iPod) may be deluding themsleves. Such a fast-buck approach has the technology seller helping themselves at their customers long-term expense…almost becoming parastic. Investors and entrepreneurs take note: the new stack won’t tolerate old stack micro-monopolies: plan on more Schumpeterian creative destruction.

In the end, it is all about risk-sharing: stack buyers that don’t perform adequate diligence, risk being marginalized by lock-in. At the same time, stack sellers that cannot constantly adapt to the marketplace will become riskier bets.

Just make sure you’re not stuck with them.

[UPDATE: AdExchanger had an intro which didn’t quite capture the point. Whether you buy a la carte or bundled technologies doesn’t matter. What matters is how those technologies integrate (or don’t) with each other and how easily you can test them. Tag management/data sharing technologies (especially pure-plays) can mitigate the inflexibility of tag based lock-in.]